This is Part 2 of our two-part series on the urgent need for banks to transform their branch networks to adapt to changing consumer behavior and expectations, competitive pressure, and financial dynamics. Part One details the trends, issues, challenges, and opportunities impacting branch network usage and performance. This article suggests a six-step approach to guide transformation activities. Contact Rolland Johannsen for information on CPG’s Branch Optimization services.

In Part One of our series on branch network transformation we made the argument that bank branches, while declining, are not disappearing any time soon. In fact, there is considerable research to support the argument that branches continue to play a critical role in the fight to capture higher shares of the highly sought after consumer deposit market and drive both balance sheet and market share growth. One only need look to the increased de novo branching activity of some of the nation’s largest banks as evidence of the connection between branch expansion and increased deposit, market, and wallet share. In our view, therefore, the question is not whether branches will continue to exist but rather how to convert them into powerful weapons in the battle to create competitive advantage, acquire new customers, capture market share, and help the bank achieve its overall growth objectives.

Over the past 20 years, retail banking executives have pursued numerous approaches and systems to help configure and manage branches and branch networks to address changing consumer behavior patterns, deploy new types of technology, and respond to increased cost pressure and shrinking retail banking profit margins. Many of these approaches combine extensive data on market characteristics and individual branch performance to target expansion, performance improvement, and (occasionally) closure/consolidation opportunities. These systems have proven effective in helping banks (especially large banks that have grown primarily through acquisitions) make incremental changes and improvements to the size, configuration and performance of their branch networks. We expect that the development and use of these types of analytical approaches will continue.

In addition to the expanded use of analytical models, many banks have experimented with new types of branches and branch configurations. These range from the development of a “Financial Supermarket” prototype by Bank One (currently Chase) over 40 years ago, through the expansion of supermarket branches in the ’90s, and the introduction of fully (or mostly) automated facilities. These initiatives have met with limited success and have proven difficult to sustain and expand across networks comprising highly disparate branch types, sizes, locations, and configurations. The cost alone to retrofit legacy branches with new designs and traffic flows has proven impossible to support both financially and strategically. Nevertheless, we expect branch design experimentation and innovation to continue within highly targeted geographies rather than across entire networks.

We also expect resource allocation challenges to continue. Over the past decade or so, most banks have invested considerable time and money to expand and transform their digital channel capabilities and processes to adapt to fundamental changes in consumer expectations, preferences and behavior. There is no indication that these investments in digital transformation will slow, let alone stop. However, in a world where resources are limited and retail banking returns are under pressure, it will become increasingly difficult to create compelling business cases to support significant investment in the branch network.

Branch Network Transformation is Primarily a Management Challenge

These initiatives and others have contributed to incremental improvements to the performance of the branch network as well as the retail distribution system overall. However, they have not been sufficient to drive needed fundamental change. The reason is straightforward: creating high-performing branch networks is not truly a design or technology challenge, but, first and foremost, a management challenge. And some would argue that it is the most difficult management challenge in the entire bank. After all, no other business line involves the sheer number and variety of customers, products, regulations, risks, policies, procedures, and employees as retail banking in general and branch channel management in particular. This diversity creates significant challenges for executives who must choose among a broad range of options for deploying their increasingly scarce resources to achieve optimal results, drive consistent behaviors, and optimize performance across this highly diverse environment. As a result, it is easy to get distracted and spend too much time, energy and money on non-value-added activities and administrative tasks. In short, there are many things that retail and branch executives could do. The challenge is determining what they should do.

In our view, the key to managing this complexity and driving exceptional and consistent branch network results is to simplify the management model. The goal is to create a management system that creates consistency by designing a set of standardized branch models and providing flexibility in how and where those models are deployed. While there are several ways to approach this management challenge, we suggest a six-step approach.

- Focus on network transformation to drive branch transformation

- Use simplified analytical models to target market-level opportunities and high-potential focus areas

- Create market-driven categories to design strategies and tactics

- Develop and install branch operating and management models for each category type

- Use branch-based technologies (including AI) to support and enhance in-person interactions, not replace them

- Align integrated sales and marketing programs and campaigns with market categories

1. Effective Branch Transformation Starts with Network Transformation

Initiatives to improve branch performance too often begin (and end) with activities related directly to how individual branches are configured, staffed, and managed. However, for most banks, branches do not truly operate independently but as a part of an interconnected network. Moreover, these networks were often built more by default than design, reflecting a history of acquisitions structured to expand geographic reach and increase market density. Over time, most banks have taken steps to rationalize and “optimize” their branch networks by applying certain concepts of network theory to network configuration decisions. These concepts, such as centrality, density, hubs, and nodes, have helped identify and eliminate clear instances of market overlap and redundancy, inform consolidation and expansion initiatives, and establish “hub and spoke” operating models.

Branches Operate As Part of an Interconnected Network

There are many analytical approaches to network theory that use sophisticated mathematical models and algorithms to understand the connections between network components and suggest optimal configurations. However, in our view, the only equation that really matters is determining whether branch presence in a defined market is configured to leverage synergies and density to achieve results that are either greater or less than the sum of the individual parts. In other words, does 2 plus 2 equal 5 or 3?

Getting the network configuration right – number, type, placement, etc. – and establishing clear network-based strategies and guidelines that drive network configuration decisions will help to ensure an integrated and consistent approach to network transformation and identify network-wide and individual branch performance improvement opportunities.

2. Use Analytics to Identify Potential Focus Areas for Management Attention.

There is a seemingly endless supply of metrics and variables that can be used to measure market opportunity and branch performance. Most banks with relatively large branch networks have combined many of these metrics into analytical models to help drive branch expansion, consolidation, and performance improvement decisions. And, for the most part, these models have proven effective in helping to sort through a large array of available alternative solutions. However, starting with these rather large and somewhat complex models may present a forest and tree problem. Rather, we often recommend a simpler initial analysis that assesses the network’s performance as a whole and identifies specific markets for more robust, complex analytical assessments.

Specifically, we look at only two publicly available data points to inform our initial assessment.

- Competitive Position – The ratio of a bank’s share of branches in a geographic market relative to its share of the deposit market within that geography. We refer to this as the ” Branch Parity” ratio. Higher ratios indicate greater market synergies and stronger competitive positions.

- Relative Growth – The degree to which the bank has grown its branch-assigned deposit balances over a designated period (we use 5 years) relative to the market growth over that same period.

We use a proprietary algorithm to combine these two variables into an index that can be applied to a bank’s network as a whole, as well as individual markets. Banks that rate high on this index can improve overall performance by focusing on a relatively few underperforming markets, while those rated low may have to rethink the configuration of their broader network.

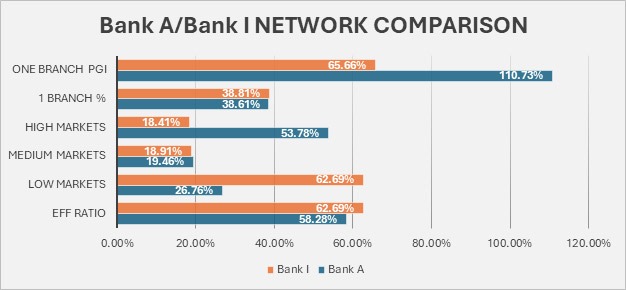

To illustrate this point, we looked at 9 Super Regional banks with large branch networks and calculated a Parity/Growth Index (PGI) for each. (Note: We do not currently provide consulting services for any of these institutions.) These banks operate over large geographic areas, and most have grown substantially through acquisition. While recognizing that there are some differences between business models, strategic focus areas, and balance sheet management priorities, there is enough similarity between these companies to provide interesting insights.

Source: CPG analysis of FDIC and S&P Global data

Based on this analysis, there are significant performance differences across the branch networks of these banks, which may require different approaches and solutions. Taking a deeper dive into the networks of the top-rated (Bank A) and lowest-rated (Bank I) networks, it becomes clear that the types and scope of improvement alternatives for each are significantly different.

Source: CPG analysis of FDIC and S&P Global data

For example, It is interesting that both operate only one branch in 38% of the markets (in this case counties) in which they maintain a presence. But that’s where the similarity ends. 55% of Bank A’s markets are rated high (over 100 PGI) while 63% of Bank I’s are rated low (under 70 PGI). This difference is also reflected in the performance in those markets where they operate only one branch – 111 PGI for Bank A in one-branch markets vs 66 PGI for Bank I. Based on this rather high-level analysis, it appears that Bank A can target a relatively few low-performing markets, while Bank I may have to take a more structural approach, including a deep-dive evaluation of single-branch markets across the entire network. It is also worth noting the differences in the Efficiency Ratios of the two companies. While a myriad of factors impacts a bank’s efficiency ratio, the branch network represents a significant cost component, so branch performance characteristics likely have a measurable impact on this metric.

3. Create Market-Defined Categories

Banks that have built even relatively small branch networks generally operate within and across multiple types of markets with varying demographic, economic, and competitive characteristics. This market-level diversity makes a “one size fits all” structural and management model ineffective. It also makes individual branch models impractical. One approach is to create a few branch categories that can be deployed to align with specific market and competitive characteristics and opportunities.

Creating branch categories is neither a new nor particularly unique concept. Hub-and-spoke models, as well as the designation of various branch “tiers,” have been around for decades. Often these categories are defined by branch size and are used to determine types of staffing, management responsibilities, etc. For example, a “hub” branch may contain certain product specialists (e.g., mortgage, wealth management, small business, etc.) while a “spoke” branch does not. Likewise, tiers have been used to establish management levels (e.g., Manager I, II, etc.), staffing composition and job grades, performance metrics, and other factors that align with the size and configuration of individual branches.

These types of category definitions have proven effective in organizing relatively large and complex branch networks into more manageable components. They have also helped to streamline management structures and provide career paths for branch employees. Enhancing and expanding the usage of branch categories will play an essential role in reducing the complexity inherent in managing medium and large branch networks, creating consistent and expedited decision-making frameworks, and driving both revenue and efficiency improvements. While there are many ways to define and design market and branch categories, in our view the key elements include:

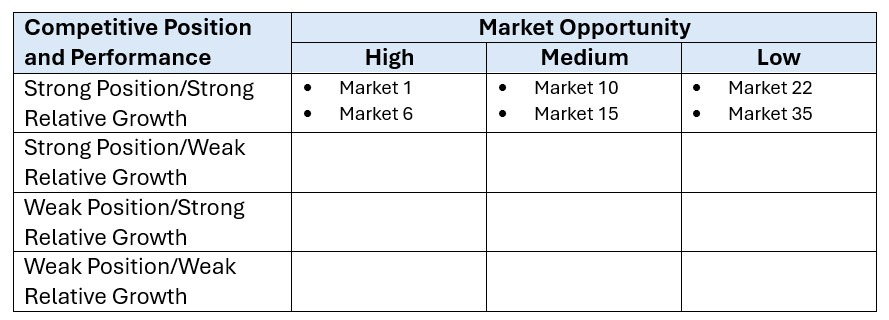

- Create consistent market definitions – identify the geographic boundaries that are used to organize network components (e.g. county, SMSA, etc.). These market definitions should be large enough to incorporate multiple branches that work together to create market synergies and brand awareness. For larger banks we generally recommend starting with county level definitions.

- Start with market categories, not branch categories – use simple metrics to create market categories. We suggest some variation of competitive position/presence and relative growth (e.g., dominant market position/low relative growth). Plot markets along each dimension to determine appropriate category assignments.

- Assess each market in terms of opportunity or “attractiveness” – identify key variables that align with the bank’s strategic priorities (growth trends, market demographics, business composition, product usage, etc.), collect available customer and market data, and develop an analytical model to assign a rating to each geographic market. While many variables can be included in these models, the goal is to create a consistent, data-driven rating system that can be applied objectively across the entire network.

- Assign each market to a discrete category – combine the market position, performance, and opportunity analyses into market-based categories and place each market into the appropriate category. The resulting analysis might take various forms based on the metrics and data used; however, it should result in discrete market assignments.

Once all the markets have been assigned to individual categories, it is possible to create high-level strategic definitions for each. For example, high-opportunity markets in which the bank has a strong competitive position and has experienced higher growth than the market may indicate further expansion initiatives. Conversely, markets with low opportunity but with similar market presence and performance may lend themselves to maintenance-related types of strategies.

Using consistent data and analytical frameworks to define individual market categories will help to organize a relatively complex, diverse, and disbursed collection of individual branches into a more manageable network, streamline management practices, and develop a consistent set of actionable market-based strategies and programs consistent with the characteristics and opportunities of each type of market.

4. Create Branch Types and Operating Models for Each Market Category

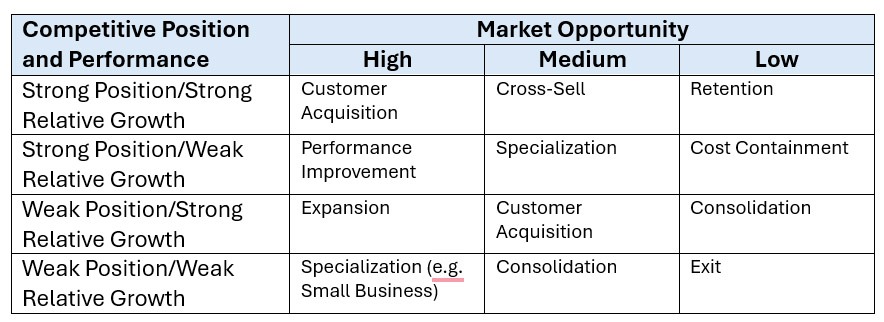

Once market-level categories are defined and assigned, it is possible to create strategic classifications for each type of market category. For example, using the types of category attributes outlined above, market classification definitions might address such issues as expansion, performance improvement, maintenance/retention, cost reduction, consolidation, and the like. These classifications can then be assigned to each market category to drive branch-related structural, management, and operating decisions.

Assign Strategic Classifications to Market Categories

These classifications can then be applied to the branches within each market. In this example, all branches within Market 1 would be classified as “Expansion” branches, whereas all branches in Market 22 would be designated as “Retention” branches.

The next, and final, step is to design management and operating models for each branch classification. The goal is to align branch-level operating capabilities and priorities with the strategic goal of each type of market. Key elements of these models might include such factors as:

- Staffing – types and levels, skill sets, training requirements, etc.

- Management structure — hierarchy, oversight, accountability and authorities

- Performance Management metrics and objectives

- Customer-facing technology installation – ITMs, self-service kiosks, etc.

Once these models are designed, they can be installed across the network to ensure that branch functionality, operating capabilities, and management processes are consistent and aligned with market characteristics.

5. Use Branch Technology to Support In-Person Interaction, not Replace It.

Over the past decade, significant investments have been made in technology to support all aspects of retail banking in general, and the retail distribution system in particular. While a number of these investments have been aimed at creating new capabilities and enhancing the customer experience, many more have been designed to streamline operational processes, support cost-reduction initiatives, and facilitate the migration of transactions to digital channels. While these investments have been necessary to address both changing consumer behavior patterns and shrinking profit margins, they have not proven sufficient to counter advancements by extremely large and non-traditional providers or develop the capabilities and processes that would lead to significant and sustainable competitive advantage.

Consequently, the need for additional technology investment will not only increase but also accelerate. However, the retail business in general, and the branch network in particular, will not be alone in requesting additional technology support. The fact is that technology demand will increase across all areas of banking, creating fierce internal competition for finite, and potentially shrinking, resources. And, unfortunately, due to many banks’ business-line accounting methodologies, other businesses and departments may be able to make more compelling business cases to support their IT requests and capture a larger share of the available technology pie. The bottom line: retail executives may only have limited bites at the technology apple, so they better make them count.

However, while resources may be limited, options on how to spend those resources are vast. Importantly, the explosion of AI-related platforms and solutions has exponentially expanded the menu of available options. This has further increased the need for retail and branch executives to be laser-focused on identifying the specific types of technology capabilities that can and will deliver the most compelling and tangible results. When it comes to optimizing the performance and contribution of the retail branch network, we believe this means aiming technology resources at those functions and capabilities that will add value to the in-person customer experience rather than replace it.

The usage of in-branch, technology-enabled devices designed to offload “routine” transactions from branch personnel has increased over the past few years but in many cases are still somewhat underutilized. For example, a recent non-vendor study puts the average number of ITM transactions at around 850 per machine/month. We expect these types of devices will continue to play a role in supporting teller types of functions and providing additional access to routine transactions outside of normal branch hours. However, the jury is still out on whether these technologies will play a significant role in offsetting more complex and value-added types of service and advisory interactions. The fundamental outstanding question is whether people who take the time and effort to travel to a branch do so to talk to a person or to interact with a machine. Therefore, the goal is to clearly and specifically identify the types of interactions that add the most value to the in-branch customer experience, and to configure technology solutions to support them.

The list of potential value-added capabilities is relatively large and goes beyond the basic functions of account opening, routine service, account maintenance, transaction processing, and the like. Rather, interactions that involve issues such as onboarding, complex problem resolution, fraud identification and mitigation, credit counseling and repair, financial management, small business support, and many others are more likely to be responsive to customers’ current and emerging needs. Once the target interactions are defined, technology decisions should consider a number of factors including:

- Data Availability and Accessibility – A major obstacle for many banks is the lack of actionable and accessible information on customers’ relationships, history, and behavior. Providing more robust and real-time data to in-branch customer-facing personnel will significantly enhance their ability to provide value-added service.

- System and Platform Integration – Progress has been made in reducing system-related silos and improving communication across the multiple applications used to support the large number of functions required to operate the retail banking business. However, considerable work remains to further integrate systems to manage customer relationships more effectively, track interactions across product types and delivery channels, manage risks, and overall create a more holistic customer experience.

- Training and Empowerment – While not truly a technology issue, the fact is that a technology solution is only as good as a person’s ability to use that technology, and the extent to which the technology empowers an employee to make informed decisions tailored to individual situations. The ability and authority to make decisions on matters such as fee waivers, policy exceptions, pricing variances, fraud resolution, and many other customer-related issues are critical to leveraging the branch channel to achieve competitive advantage relative to both in-market and non-traditional providers. Technology plays an essential role in supporting empowered decision-making while also providing management with the tools to track and monitor exception volume to identify potential abuse.

All in all, we expect the role of technology in transforming the branch network and optimizing performance to continue to increase. Further, we expect the expansion of AI-powered solutions and use cases to accelerate as the technology evolves and managers become more aware of and comfortable with its use. In our view, the winners will take a very focused approach to technology investment and implementation by understanding not only what the technology could do, but also identifying what it should do, and then making a clear-eyed assessment of what the organization can do in terms of resource capacity and implementation capability.

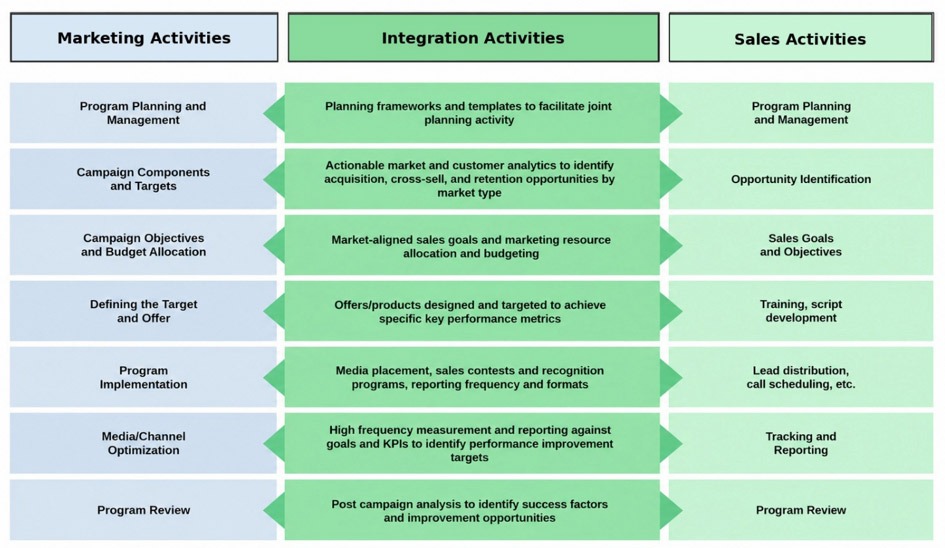

6. Align integrated sales and marketing programs with Market Categories

Transforming the branch network into a high-powered asset that drives growth and achieves competitive dominance requires developing and implementing integrated, market-aligned marketing and sales programs. Too often, marketing and sales programs are conducted independently of each other, have different objectives, and do not operate using the same data or analytical frameworks. The result is often suboptimal performance and, potentially, internal conflict.

In our experience, the winning strategy is to view marketing and sales as two sides of the same coin rather than separate functions. This means engaging in joint planning, utilizing the same data to identify and quantify opportunities and set objectives, developing consistent marketing creative and sales collateral material, fully integrating target marketing algorithms with lead distribution processes, and implementing unified tracking and reporting frameworks.

Creating integrated sales and marketing programs and campaigns has proven effective in producing significantly higher results than sales and marketing campaigns conducted independently. We have found that, if done properly, this integration can be a critical element in supporting branch and branch network transformation initiatives, converting branches from cost centers to revenue engines, and strengthening both brand awareness and competitive position.

While these integrated programs can help produce tangible results, the real power comes from aligning program features – offers, lead lists, performance metrics and objectives, reward and recognition programs, etc. – with defined market categories and incorporating a systemic integration process into the branch network management model. The resulting process will help to ensure that marketing and sales programs work together on an ongoing basis to support and enhance branch network transformation and performance improvement initiatives.

Nobody Said This Would Be Easy

There is considerable evidence that the number of bank branches is shrinking, and that both the volume and type of branch traffic are changing. Shifts in consumer behavior and preferences, enhanced technology capabilities and utilization, evolving competitive dynamics, and many other factors are putting pressure on retail banking executives to make fundamental change to how the branch network is configured and managed. However, with all these changes and with all this pressure, there is no indication that branches are going away anytime soon. Therefore, doing the hard work and creating a comprehensive approach to branch and branch network transformation will be a critical strategic priority for most banks to turn a legacy, and potentially dormant, asset into an engine that can drive growth, create competitive distinctiveness, and generate significant financial returns.