This is the first in a two-part series that addresses the urgent need for branch network transformation. This article focuses on the reasons why transformation is necessary and lays out the challenges to implementing fundamental change. Part Two provides additional context and suggests a six-step approach to implement an effective branch network transformation process.

Over the past few decades, bank branches have been characterized as superfluous, anachronistic, inefficient, unnecessary, and a host of other adjectives that support the argument that branches and branch networks have no place in an increasingly digital world and should be put out of their misery. Supporters of this position point to significant declines in branch traffic, changing demographics, Covid-driven behavioral shifts, the increased sophistication of digital channels and capabilities, the success of online providers, an increasing focus on cost reduction, and a number of other factors that are undeniably true. Yet, branch networks continue to not only survive, but by some metrics thrive. To paraphrase Mark Twain, “The reports of the death of bank branches have been greatly exaggerated.” The question is “why”?

Branch Usage Statistics Paint a Grim Picture

Anybody who has been paying attention knows that there has been a dramatic shift in how customers choose to interact with their bank, complete transactions, open accounts, and perform routine account maintenance and service functions. And, while many of these trends were visible during the last decade, all of them were put on steroids during the Covid era as people were forced to isolate, branch visits became a hazardous outing, and customers who were not digital natives were forced to learn how to navigate online and mobile platforms. In fact, a case can be made that Covid did more for digital channel adoption and usage than all the sales and marketing activation campaigns conducted previously combined.

While natural and environmental forces were driving behavioral change, most banks were expanding and enhancing their digital capabilities and improving the online customer experience This included providing access to more transaction types and account information and, importantly, more streamlined account opening procedures. While the digital channels were receiving significant investment and expansion, one could argue that branch functionality and capabilities changed little, if at all. In fact, the only two major branch-level changes have been significant reductions in staff and increased focus on onboarding walk-in customers to mobile and online platforms.

These factors taken together have produced dramatic changes in channel usage and behavior. For example, over the past ten years:

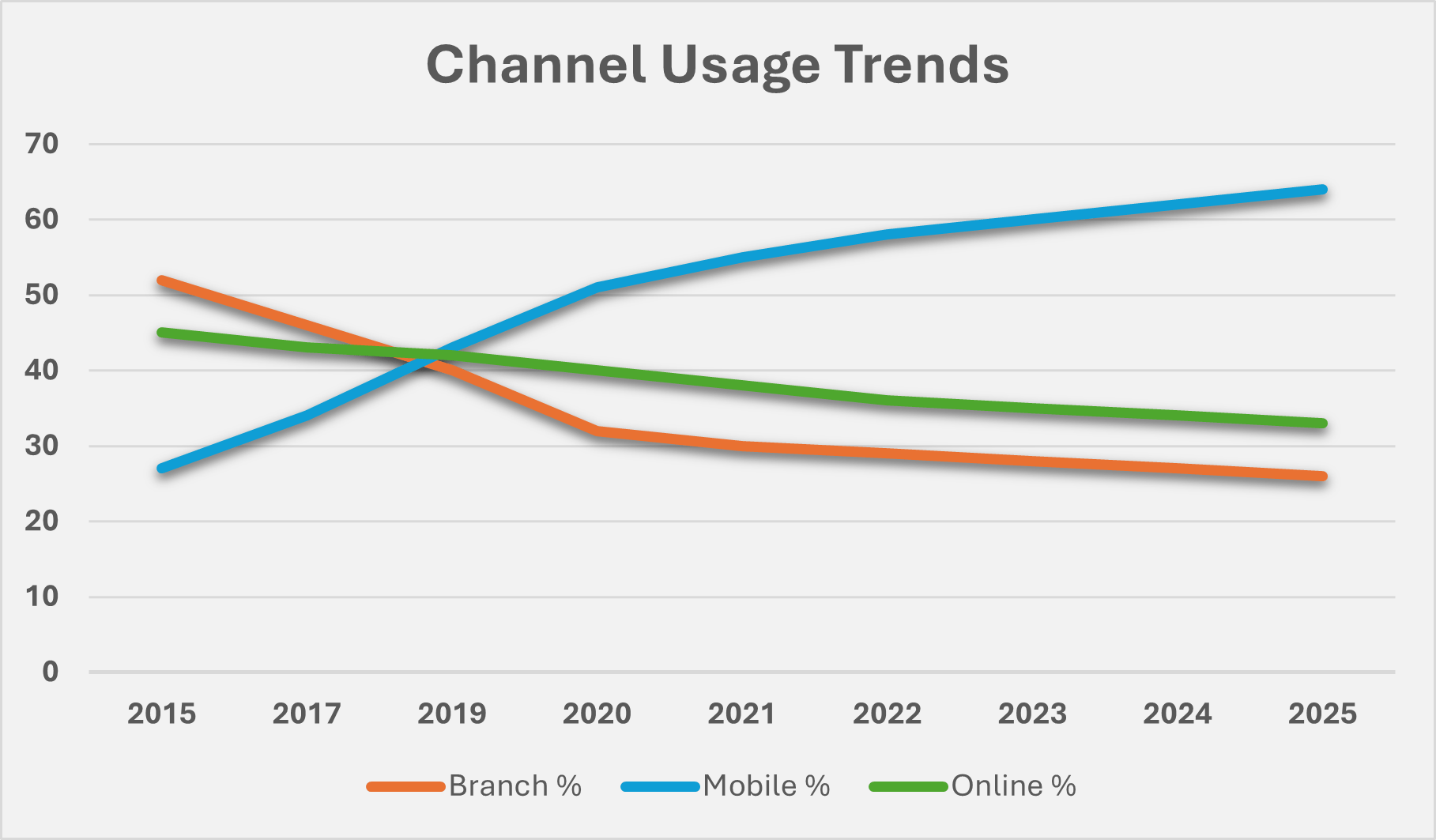

The % of customers using a branch has been cut in half while usage of mobile platforms has more than doubled.

Source: Various U.S. Consumer Banking Usage Surveys

Source: Various U.S. Consumer Banking Usage Surveys

The transaction mix has shifted more dramatically with digital channels now accounting for 84% of total transaction volume.

Source: CPG Summary of Industry Research

Source: CPG Summary of Industry Research

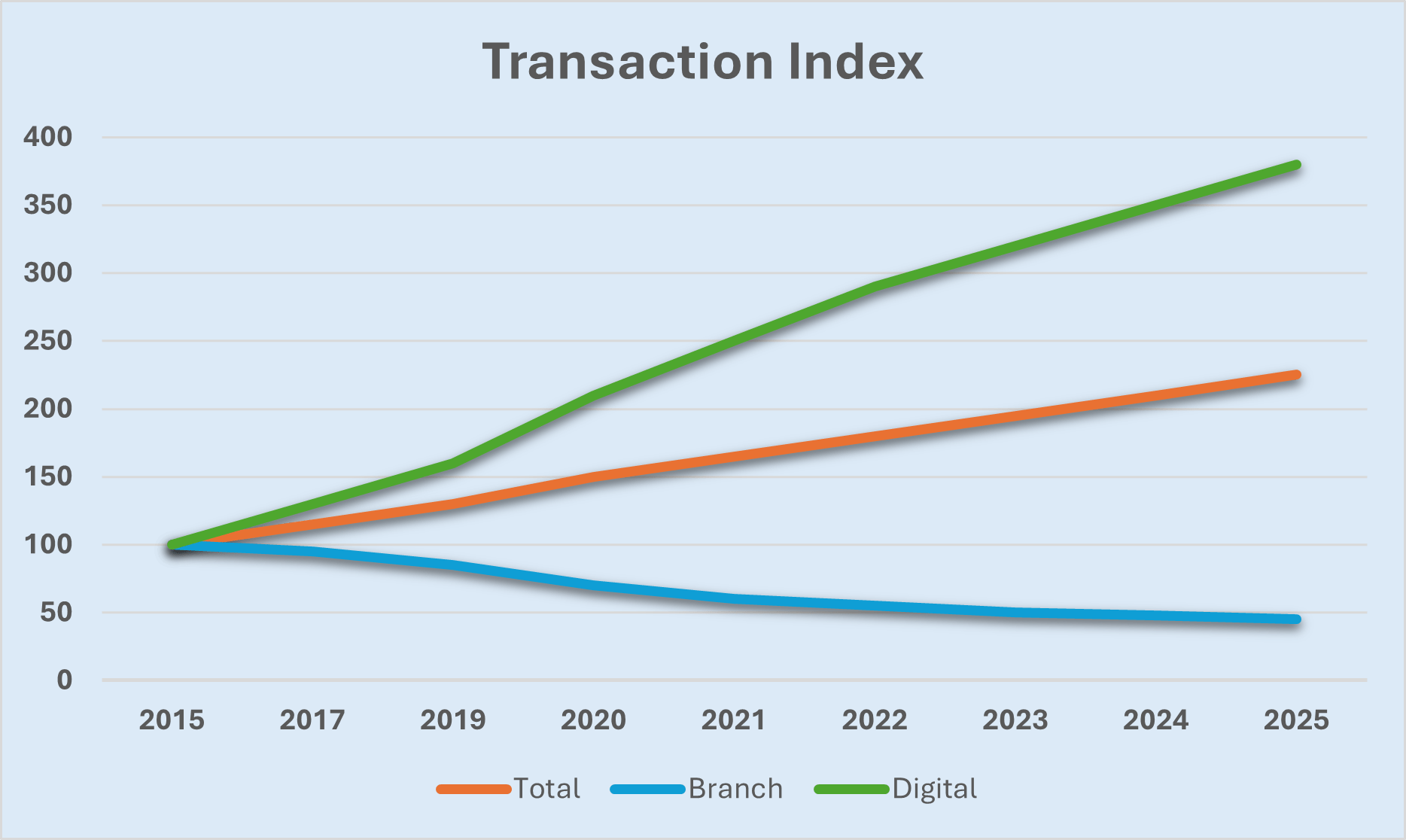

Total financial transactions have increased 225% while the branch index has declined by 55% and the digital share has increased by 380%.

Source: FDIC Bank Activity Trends, FRB of St. Louis payments/transaction data

Source: FDIC Bank Activity Trends, FRB of St. Louis payments/transaction data

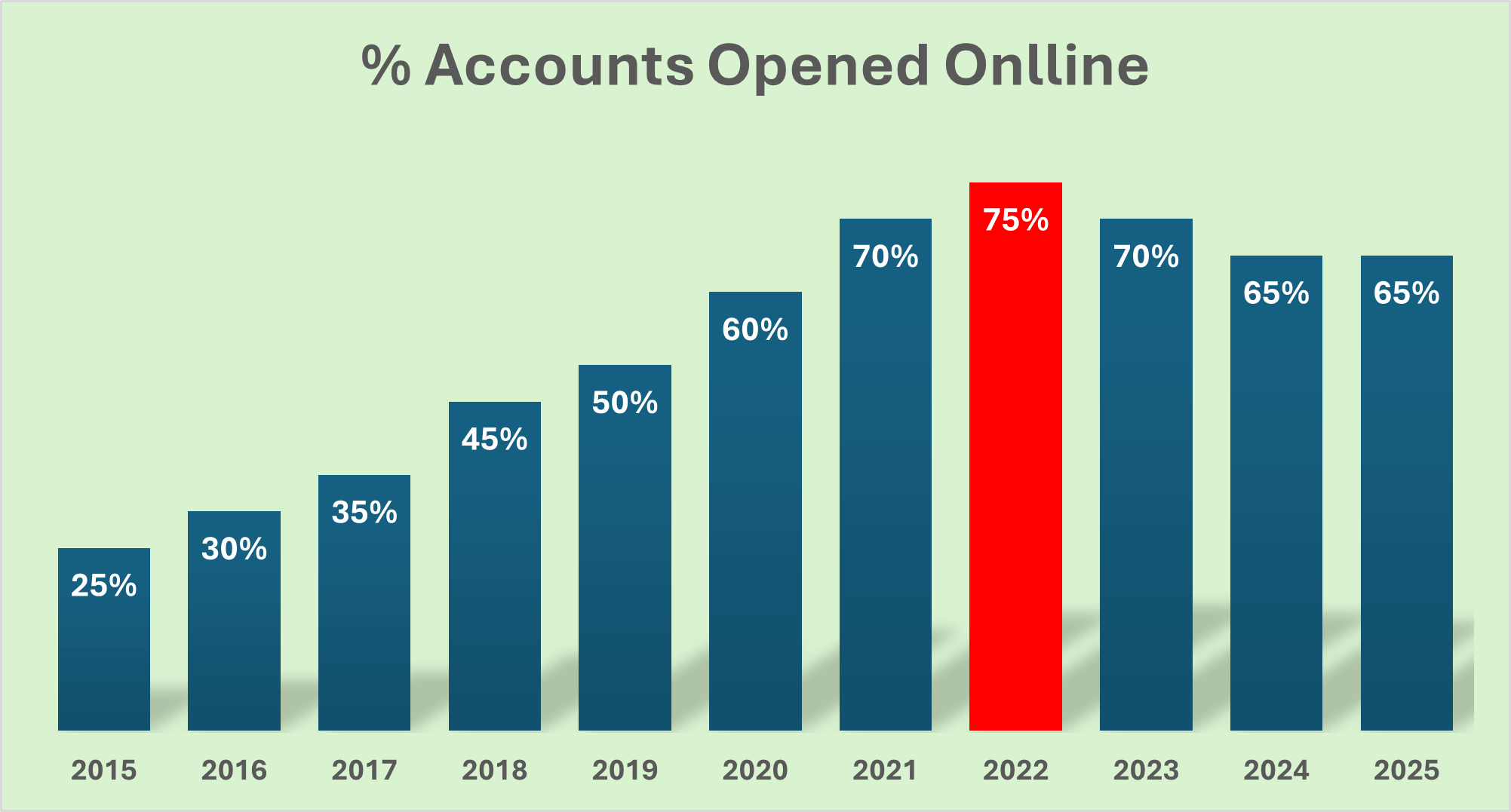

The percentage of new accounts opened online has grown exponentially.

Source: CPG Summary of Industry Research (ABA, BAI, FDIC)

Source: CPG Summary of Industry Research (ABA, BAI, FDIC)

There are many other statistics and data points that support the argument that branches have become a minor and less relevant channel to acquire and serve a broad range of customers. All these trends and others have followed a similar pattern over the past ten years – changes accelerated into and through the pandemic period and leveled off somewhat since. The jury is still out, however, if current volumes represent a sustainable floor or if adoption of new technologies such as AI will kick start additional behavioral shifts and further accelerate the movement into digital channels.

This is not exactly breaking news, especially to those who are charged with configuring and managing large branch networks. Most retail banking executives are fully aware of the need to address the role and performance of their branches as part of their mandate to create and manage multi-channel retail distribution networks that are cost effective, deliver a superior customer experience, establish competitive distinctiveness, and support the bank’s growth and profitability objectives. And over the past decade many have committed additional time and resources to a variety of initiatives to address these clear trends. These initiatives go by a number of descriptive names but often include:

- Channel Integration: providing similar processes and customer experience across and through all delivery channels.

- Omni-Channel Delivery: Creating seamless interactions, information flows, and experiences across all channels.

- Branch Automation: Installing technology-based devices (e.g. ITMs, self-service kiosks, etc.) within branch facilities to offload routine transactions onto self-service platforms.

- Integrated Sales and Marketing Programs: Highly targeted campaigns that seek to create synergies between marketing programs and branch-based sales activities.

- Network Optimization: Data-driven programs to identify branch consolidation and closure opportunities.

- Digital Transformation: Expanding digital functionality, streamlining processes, creating seamless customer experiences, and increasing activation and usage.

- Branch Transformation: Transitioning offices from transaction facilities to sales and advisory hubs.

While there have been some notable exceptions, many of these programs have met with limited success and have often been abandoned. Obstacles to making fundamental changes to the branch network have proven formidable.

- Legacy systems, policies, and processes are typically inflexible and have proven difficult and expensive to change.

- Bank accounting systems often undervalue the financial contribution of the retail business line, making it difficult to create compelling business cases to compete for and secure scarce technology and other capex resources.

- Most banks have been reluctant to change compensation systems and significantly increase branch-based employee salary ranges and job grades to support expanded roles, responsibilities, and skill sets.

- Access to real time customer data is often limited, making it impossible to support a true omnichannel strategy.

- Branch networks (especially large networks) have been built up over time and are composed of a wide variety of types of branches with varying sizes and physical layouts. Retrofitting these facilities to accommodate new roles, technology platforms, and traffic flows is costly, time consuming, and often physically impossible.

- Utilization of branch-based self-service devices is inconsistent across the industry making it difficult to justify substantial purchase, installation, maintenance, and operating costs.

- Marketing programs and competencies have often outpaced sales and sales management capabilities, often leading to suboptimal campaign results.

These roadblocks and others have made it difficult and frustrating to make the kinds of fundamental changes necessary to address systemic changes in customer behavior, channel usage, and branch network financial dynamics. And, while change may prove difficult it is nevertheless necessary for the simple fact that despite pundit prognostications over the past few decades, branches remain a large and important component of most banks’ delivery channel mix.

Branches Will Continue to Decline, Not Disappear

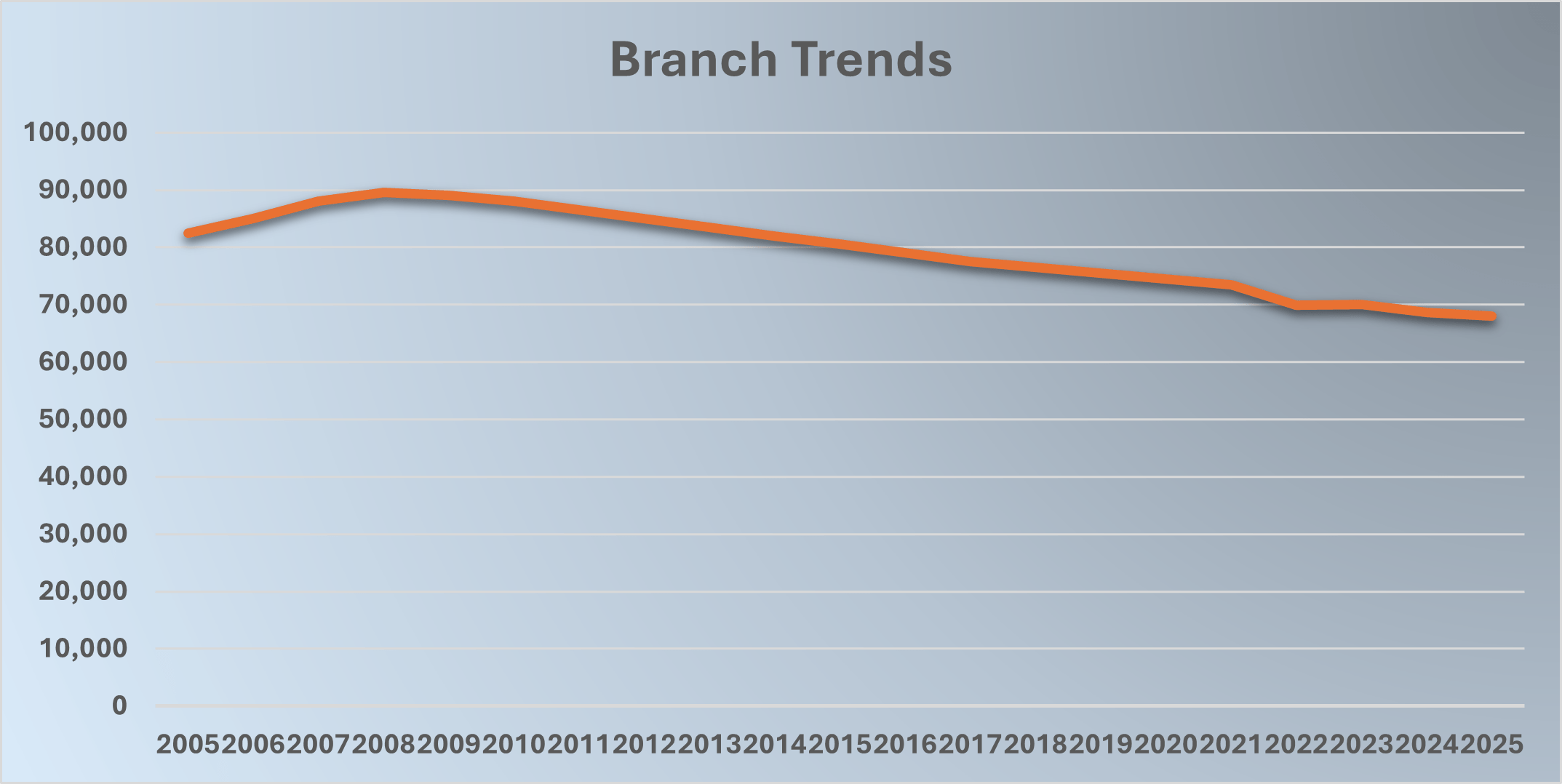

The reduction in the number of bank branches over the past twenty years has been well-documented. From a peak of around 89,000 during the financial crisis, the number of branches has steadily declined to approximately 68,000 at the end of 2025, a reduction of just over 20%.

Source: FDIC Commercial Bank Branches

Source: FDIC Commercial Bank Branches

In addition to the customer behavior and channel usage trends described above, other forces have helped drive this steady decline.

- M&A Activity: Consolidations between relatively large Regional and Super Regional banks both during the financial crisis and more recently have caused surviving entities to eliminate overlapping branches, exit low opportunity markets, and take other branch-related actions to help achieve merger-related expense synergies.

- Balance Sheet Management: A sustained period of low interest rates, relatively low loan demand, and excess liquidity put pressure on margins and reduced the appetite for higher cost retail deposits. Branch closures were accelerated to help reduce costs and maintain acceptable shareholder return.

- Ongoing Network Optimization and Configuration: Many banks, especially those with relatively large branch networks, have installed data-driven models to identify branch closing and consolidation opportunities and priorities.

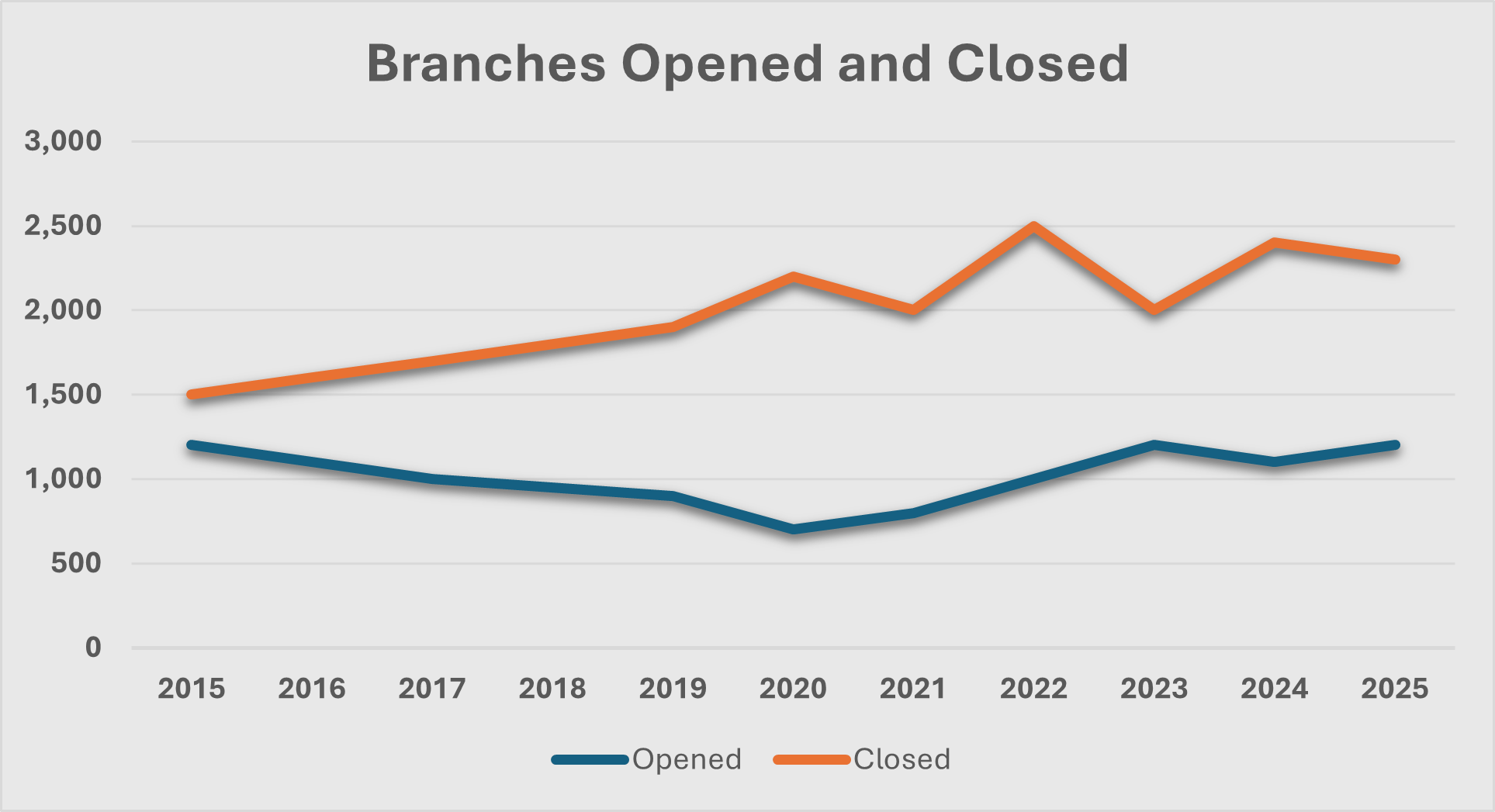

We expect both continued industry consolidation and ongoing network optimization activities to further reduce the number of branches over the next few years. If history is any judge, the impact of accelerated M&A activity between larger banks may have the most profound impact. During the period 2019 to 2022 there were eight mergers between banks that each had over 100 branches. Since the mergers were closed, these institutions have reduced their combined branch totals by just over 2000 branches or approximately 18%. It is not surprising that those banks with the largest combined networks saw the largest decreases.

Source: FDIC, Company Reports

Source: FDIC, Company Reports

It is likely that more recent large bank consolidations will produce similar types of branch reductions.

While acquisitions and ongoing cost reduction programs will drive further closures and consolidations, we expect these to be offset somewhat by the increasing need to build, expand, and maintain stable core deposit franchises. It is our view that branches can and should be a powerful weapon in the battle for stable, low-cost deposits. It appears that some banks agree as the number of new branches opened over the past three years has reached and exceeded pre-pandemic levels. And while the net number continues to decline, we expect targeted branch expansion to continue. It is interesting to note that the very largest banks (specifically Chase, BofA, and Wells) have been the most active recently as they enter new markets or expand into high potential existing markets through de novo branch expansion rather than acquisition. These very large banks have also been the clear winners in the fight for retail deposit customers, accounts, and balances.

Source: FDIC

Source: FDIC

The importance of the branch as part of an overall deposit strategy cannot be evaluated solely on the basis of branch traffic, transaction volumes, or suboptimal sales results. Rather, there are other factors that support the branch as a critical component of both customer and deposit acquisition strategies. Key among these is that branch presence continues to rank high as a selection criterion for deposit-rich segments such as older customers and small businesses. Additionally, branches provide a physical representation of the bank’s brand. This increased and constant brand awareness helps support other lines of business such as commercial, and powerfully reinforces the bank’s image as an integral part of the community.

Branches: Can’t Live With ‘Em, Can’t Live Without ‘Em

It is likely that the debate regarding the value, viability, and relevance of branches and branch networks in an increasingly digital world will continue. And, while this is an interesting debate, it is the wrong one. The fact is that there remain a large number of bank branches, and they are not disappearing any time soon. And, while banks will (and should) continue to use increasingly sophisticated models to optimize the number of branches within their geographic footprint, it is neither financially, competitively, nor strategically feasible to reduce branches below a certain threshold number, let alone eliminate them completely. Consequently, the question is not whether branches will continue to exist but rather how to convert them into a powerful weapon in the battle to create competitive advantage and distinctive value propositions, acquire new customers and capture market share, expand and solidify customer relationships, and contribute significantly to the bank’s overall financial performance. In short, when it comes to branch network strategy our advice is “smoke ‘em if you got ‘em”.

Part Two of this series suggests a six-step process to address the management challenges Retail Banking Executives face to transform the branch network into a powerful and cost-effective asset that can help drive profitable growth and create significant competitive distinctiveness.