Community banks are facing a long-term decline in a core segment: small business lending. To reverse the decline, they must enhance digital technology, adapt their processes, and build on their competitive advantages.

What the Data Shows

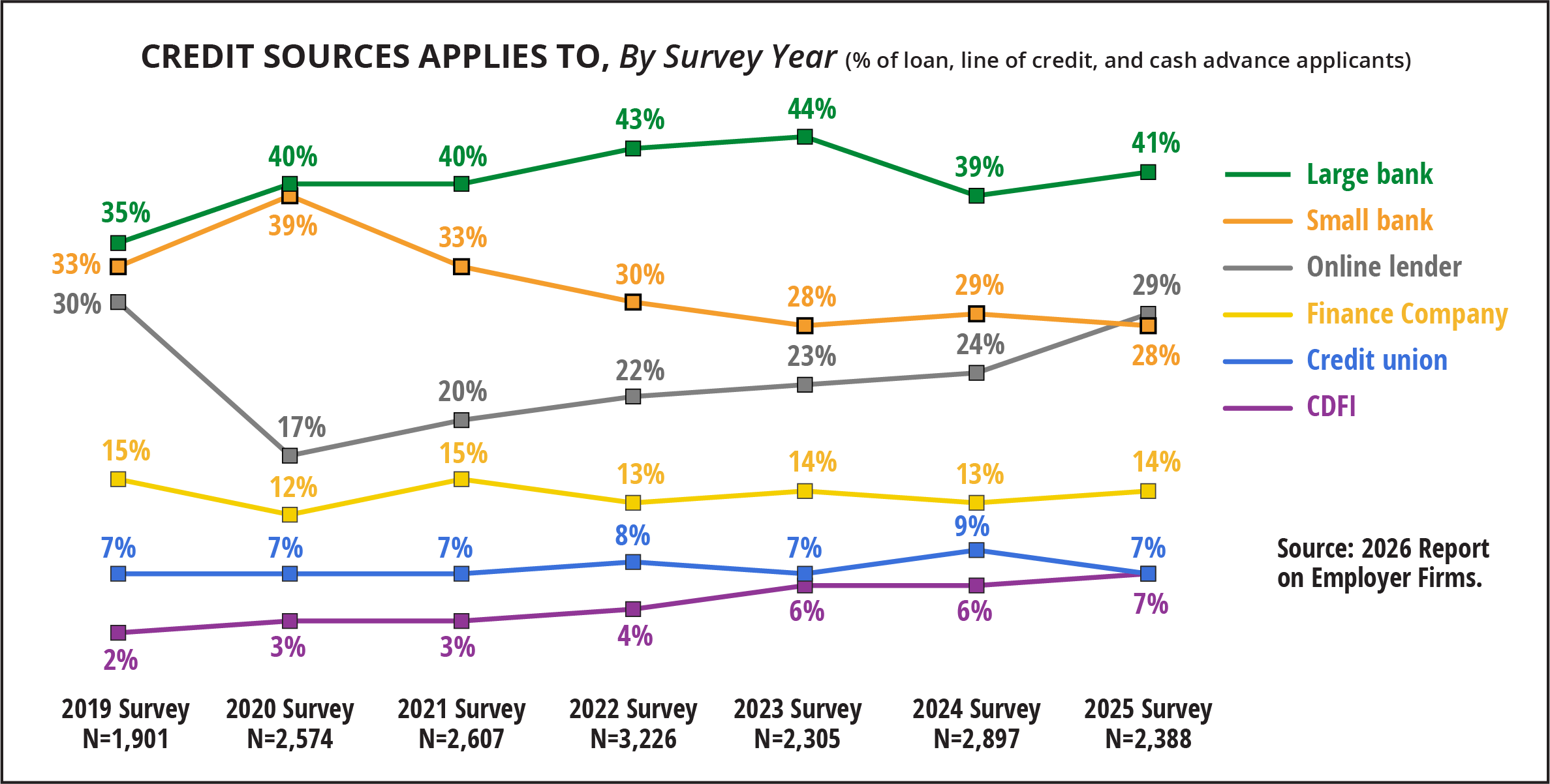

According to the Federal Reserve Banks 2026 Report on Employer Firms, 38% of firms with fewer than 500 employees applied for loans, lines of credit, or merchant cash advances last year. That percentage was consistent with prior years. However, the survey highlighted a marked shift regarding where applications were being submitted.

Other than an increase in small business applications in 2020 due to the Paycheck Protection Program, the share sourced by community banks has steadily declined. A separate 2024 study by the Federal Reserve Bank of Kansas City reached a similar conclusion. An examination of the competition for small business loans provides insight into the reason for the decline.

Who is Taking Share and Why

Large banks are the dominant source of credit for small businesses. On average, they source 4 out of every 10 small business loan applications. Their market position is secured by leveraging operational scale and investing heavily to retain and grow their share in this attractive relationship segment. For example, JPMorgan Chase recently announced a major initiative targeting small businesses, with a 10-year goal of acquiring 3.0 million new small business customers and originating $80.0 billion in loans, both directly and through partners such as CDFIs.

Online lenders compete via speed and digital ease. A combination of fast processing, convenience, and smooth digital experience has enabled online lenders to achieve significant growth, even though their borrowers are more likely to pay higher rates or experience service issues. The share of small business applications submitted to online fintech lenders rose from 17% in 2020 to 29% in 2025, surpassing that of community banks.

Credit unions pose a threat as their tax-advantaged status affords them a pricing advantage over community banks. Though business lending remains somewhat nascent at credit unions, they continue to grow their loan outstandings. Aggregate net member business loans outstanding rose from $51.3 billion in 2015 to $181.5 billion in 2025, equating to a 13.5% compound annual growth rate. While their share is modest today, it will grow as larger credit unions continue to build out their business lending capabilities organically and through acquisition.

Community banks possess competitive advantages as well. Often, they pursue a relationship-oriented, geographically focused approach to lending that is rooted in knowledge of and history with their customers and communities. They compete with a combination of high-touch service, accessibility and responsiveness, underwriting customization, and banker expertise. They have a competitive advantage over large banks by working closely with customers who need guidance and assistance in the lending process. Their deeper, multiproduct relationships with borrowers enable them to offer better loan rates than online lenders.

Indeed, this approach and positioning have distinct strengths. The Fed survey of employers found that small banks had higher full-approval and borrower net satisfaction rates than other lenders. These strengths are real, but insufficient on their own, as evidenced by the downward trend in the share of applications.

What Community Banks Should Do

To recapture share, community banks’ legacy strengths must now be combined with process simplification and selective technology enablement. Simpler underwriting and documentation requirements should be instituted for small business lending, rather than the complex requirements of commercial lending. Developing deep expertise in specific local industries can be leveraged to offer loan terms that automated fintech models might miss, and potentially to similar prospects beyond the bank’s local geography.

The application process should be simplified by collecting only essential data and utilizing e-signature tools. AI can be deployed for repetitive tasks such as document intake, data extraction, ID verification, and fraud detection to expedite processing and free up staff for high-value advisory work.

To offer better pricing on the loan portion of the overall relationship, community banks must have the tools to measure the relationship’s full profitability, including deposits, merchant services, and cash management solutions.

Client-facing digital tools should be integrated with banking platforms to help small business owners save time and improve productivity. Online account management tools, such as cash flow forecasting, expense reporting, invoicing, fraud protection, and security, reduce manual work for time-constrained business owners and improve engagement and loyalty. The bank’s website content should clearly communicate product features and their value.

Digital tools and technology enhancements can also help to strengthen, rather than replace, personal relationships. AI can be used to analyze customers’ and prospects’ financial statements, summarize key trends, and generate discussion points for relationship managers, enabling them to focus on high-value, face-to-face interactions and relationship-building. Customer communications should include personalized offers and notifications, such as meeting scheduling with a relationship manager. Video conferencing, secure messaging, and personalized business advisor portals enable banks to connect with clients in a convenient yet meaningful way. Digital marketing campaigns should be used to raise market awareness and consideration of the bank.

Conclusion

Competition in small business lending has changed: borrowers value speed and digital convenience. While the personal touch of relationship banking remains critical to the value proposition of community banks, they must augment human interaction with technology. This “relationship-plus-tech” position will provide community banks with the edge to outpace competitors.

Contact Claude Hanley for more information on small business lending, and visit our Sales and Marketing and Strategic Planning practice area pages.