The banking industry recorded strong financial performance in the third quarter of 2025, and early signs suggest fourth-quarter results will be strong as well. Net interest margins expanded for the fifth consecutive quarter. Analysts and investors are now bullish on the banking sector, driven by expectations of a steepening yield curve, continued economic growth, and solid credit fundamentals. Executives at many banks noted consumer resilience and steady commercial loan demand as factors expected to support continued loan growth through 2026.

Yet a note of caution should be sounded amidst this optimism. Deposit growth lagged loan growth, particularly among institutions with total assets under $10 billion, which constitute 96% of all banks. While some banks achieved double-digit organic deposit growth, upon closer examination, they did so by relying on brokered deposits or CDs. The deposit challenge isn’t something new. The last decade has made clear that deposits are one of the most significant challenges facing the industry.

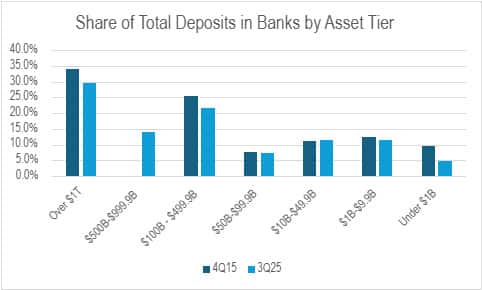

The Last Ten Years

Over the last ten years, annual deposit growth for the banking industry has averaged just 4.8%, while the number of banks declined from 6,191 to 4,388. Virtually all deposit growth occurred at the largest banks in the country – those over $500 billion in assets – at the expense of smaller institutions. Deposit growth in these larger banks was driven primarily by M&A, perhaps alongside modest organic growth.

In 2015, there were no banks in the $500 to $999 billion asset tier. By 3Q 2025, there were five: US Bank, Capital One, Goldman Sachs, PNC, and Truist, and these banks combined for $3.2 trillion in deposits, 22% of total industry deposits.

- Data sourced from FDIC as of February 2026. Includes all FDIC-insured banks, analyzed at the subsidiary level.

- Core deposits are defined as Total Domestic Deposits, less Time Deposits.

By the end of 2025, U.S. money market fund assets had surged to a record $8 trillion, with much of this coming out of traditional bank deposits. It’s simply easier than ever to move liquid funds out of your bank accounts into higher-yielding money market funds, or even Treasury securities.

Over the 2015 – 2025 period, credit unions grew deposits by 6.2%, a significantly higher rate than banks. And let’s not forget the impact of neobanks and digital banks. According to Cornerstone Advisors, roughly half of all new consumer checking accounts are now opening at places like Chime, SoFi, and other digital-first competitors who offer an easy alternative to traditional banks. Core deposits at SoFi’s national bank subsidiary totaled $38.5 billion as of December 31, 2025.

The Threat is Increasing

If you think deposit competition has been tough over the last ten years, get ready for the next ten years. Competition for deposits is going to increase. A new wave of fintechs is queued up to obtain bank charters. Their ranks include established neobanks such as SoFi and Chime, segment specialists such as Mercury Technologies, and payment specialists such as PayPal Holdings. Brokerage firm Edward Jones has applied for a bank charter. And the regulators have been keen recently to grant charters. While it’s too soon to say which of these companies will succeed in the difficult business of banking, it’s reasonable to assume they will intensify competition for deposit funds.

The adoption of stablecoins by consumers and businesses poses another threat. Estimates vary, but all indicate a material impact on the banking system’s deposit base. For example, the U.S. Treasury’s Borrowing and Advisory Committee estimates up to $6.6 trillion in deposits could shift from banks to stablecoins by 2030, representing roughly 36% of total U.S. bank deposits.

Banks are losing their primary competitive advantage: access to inexpensive funding. For some, it’s an existential threat, including those banks that have:

- Consistently growing loans faster than deposits;

- A high reliance on rate-sensitive or uninsured deposits;

- Weak “primary bank” relationships (customers treat the bank as a commodity);

- Asset-side constraints (e.g., low-yielding legacy securities/loans) that limit how much the bank can raise deposit rates without crushing margins; and/or

- Been forced into expensive funding (FHLB/wholesale/brokered), which can stabilize liquidity but erodes earnings power.

In our next article, we will explore how community and regional banks can compete more effectively for scarce core deposits and primary relationships. The game isn’t over, but the playbook needs to change.

Contact Mary Beth Sullivan for more information.