American Banker BankThink

June 4, 2020

by Claude Hanley

The key factors that allowed the best banks to outperform last year included higher fee income, greater efficiency and stronger loan growth than their peers. But suddenly, we are in a very different operating environment than we were just six months ago, and the implications for banks are profound.

Going forward we expect the drivers of top performance will be dramatically different than in the past due to the upheaval from the global coronavirus pandemic.

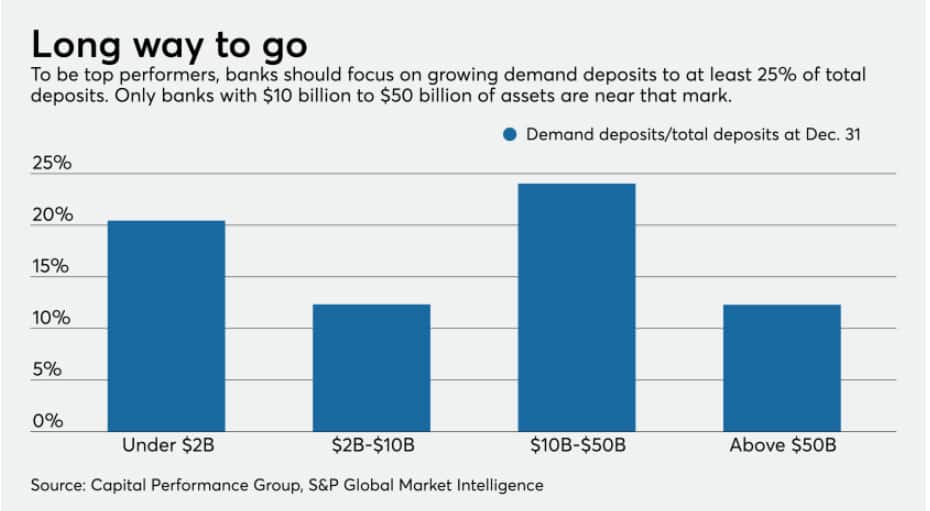

Here are six metrics that forward-thinking executives will have to focus on to thrive amid the uncertainty ahead, based on the annual analysis of bank performance conducted by Capital Performance Group and American Banker.

1. Credit quality: Credit quality was pristine in 2019, with little difference between top performers and their peers. In fact, credit quality has not been an issue that required any serious discussion in the banking industry for a decade. However, that is about to change in a big way.

Some top-performing banks have enjoyed higher margins from higher-yielding, higher-risk consumer businesses such as credit cards or exposure to business sectors that are especially vulnerable to disruption from the pandemic. But now they’ll see their level of nonperforming loans and leases spike compared to banks that were more conservative in their lending.

Credit quality will likely be the key metric in determining performance in 2020, with high performers diverging from the rest of the industry.

2. Expenses: As was the case for the past few years, top performers in 2019 had both higher revenue growth and higher growth in operating expenses compared to peers. But revenue growth is facing gale-force winds, so the top-performing pendulum is about to swing in favor of those banks that focus primarily on controlling operating expenses.